Establishing relationships is positive for the supply chain and can future-proof your roastery against price volatility. Keep reading to understand the movements triggered on the ground by the increase in the C-price, how producers in Brazil and Peru are responding to it and get sound advice from our sales manager Toom Booth.

Why is specialty going up in price with the C? Are they not different things?

Many roasters we speak to, especially new ones, think that the specialty and the commodities markets don’t mix, like water and oil. It’s true that they are separate to some extent and the higher in quality you go. However, when it comes to the lower end of specialty, the coffees cupping between 80 and 84 points, the cut is not as clear. In recent years, quality has gone up so much that these coffees are now referred to as high commercials and not treated as specialty by many producers. At times, what separates under 80s to specialty is more sorting and dry-milling than the coffee itself. There is a fine line separating these coffees this is why things can get muddled.

Commercials and high commercials are priced very closely. In Brazil, big farmers make a profit because of volume. Small farmers cover their costs and earn a small profit. In Peru, on the other hand, the normal market prices haven’t been covering the costs of production for years. Now that these smallholders can finally breathe and have enough money to invest in their farms they are faced (and I have heard it myself) with buyers accusing them of speculation and of being opportunistic. If you don’t think there is something wrong with this narrative we urge you to think again.

Why is the low crop in Brazil raising prices in Peru?

The coffee market is globalized, so what happens in one country affects all others. Now that the C-market is up, local prices have also gone up. Sometimes, they rise above the C because of other pressures in the domestic market, such as the price for staple foods or petrol going up. Cooperatives and exporters are the main sellers of high commercials on the international market. As they have to buy coffee to sell, they can’t escape the commodities price volatility.

Other than the smaller crop in Brazil, we have also seen a decline in production in many countries, especially those where the labour force has been restricted. We have seen shipping trouble with container shortages and the issue with the Suez Canal, all leading to a general reduction of coffee availability. Where there is less supply, prices go up.

As with other commodities traded on the exchange, there is room for speculation. Investment funds or highly capitalized individuals that have nothing to do with coffee buy futures to sell when the market is at its peak. Local speculators buy coffee early for cheap and resell at better prices when an opportunity appears. This happens in any country and the reason why it’s affecting Peru now is that they have coffee to sell now. More people buying shows the market more demand and this also increases the price.

Look at it from the farmers’ point of view. If their lower grade coffee that is cheaper to produce is worth more right now, why wouldn’t the same apply to their higher grades that cost more? They could sell at the same price, which many do, but they wouldn’t match last year’s prices, especially if they don’t have a relationship. If cooperatives and exporters don’t manage to sell at the current prices they simply cannot buy coffee to fulfil their orders and they risk losing money to do so. The producers are always free to sell elsewhere. And, honestly, why shouldn’t they?

Are cooperatives and exporters speculating?

In Peru more than in Brazil, the quality delivered by small farmers falls largely on the high commercial bracket without any special processing method. When growers take their coffees to the cooperative’s warehouse, they will be paid according to the local market price, which follows the C-market. Then, when the coffee is paid and if well paid, the cooperative will distribute one or two premiums. Cooperatives also rely on financing to pay these coffees upfront and assume the risk from farm to port, giving buyers more comfortable payment terms than they would have if buying directly from the farms. It’s an invaluable service. We can’t expect them to lose money.

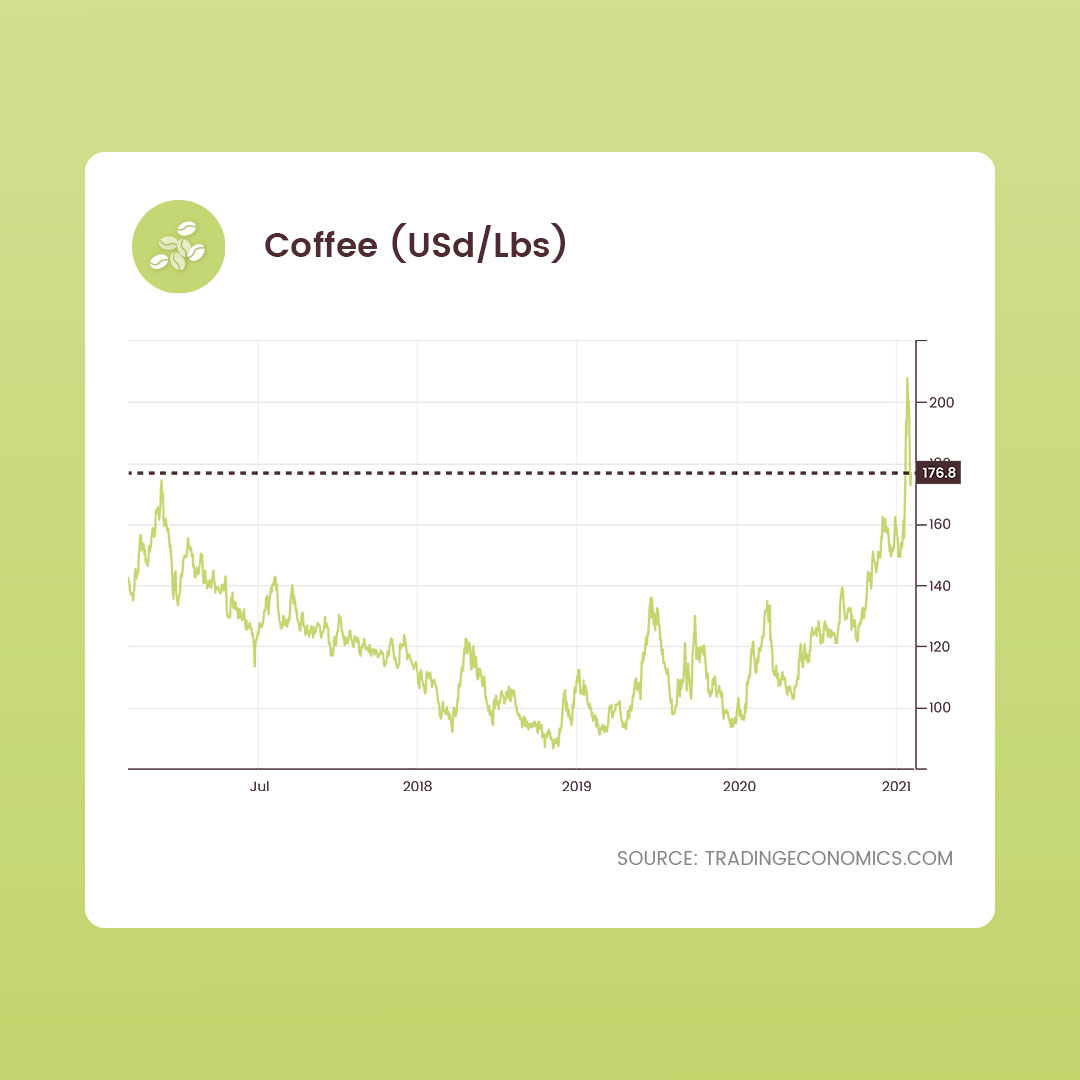

For the first time since 2014, the C-market price hit the $ 2/lb mark. That is to say base level commodity coffee is on the open market at USD 4.40/kg. Given that cooperatives look to pay premiums to keep their members loyal, they are not going to be offering coffee under. The graph above shows the C price over the last 5 years with a dotted line at today's price. Although this has dropped considerably since last week, this is still higher than it has ever been in the last 5 years. We are now seeing estate lots and cooperative blends coming up at USD 2.20/lb (USD 5/kg.)

Roasters must also consider the FairTrade minimum price as many cooperatives who are certified use it as a baseline (even if the buyer is not certified coops are still paying for the certification, audits, etc.). These cooperatives set the price of their coffee at $1.60 / lb ($1.40 / lb, which is the FairTrade minimum, + USD 0,20 / lb FT certification). It’s easy to see why large estate lots and cooperatives blends have started at $1.60 - USD 2 / lb. With the C-price below USD 1.40 / lb for the last 5 years, it has also been easy to buy large lots at or just below USD 2 / lb.

Okay. If specialty is still linked to the C-market, how can I change that?

The scenario is slightly different with large estates. They don’t have to buy coffee from other producers to price their products. However, they will not start pricing their coffee for an open sale under the market price because it puts them at a disadvantage when negotiating. If they don’t know the customer or it’s a first time customer or they don’t know that the customer will return, they have no incentive to sell cheaper. This is why relationships are so important. Loyal customers get better deals. Period.

Cooperatives and exporters who have been paying well above the market for years and have developed a strong relationship with their members or partners can also negotiate prices with more flexibility. In this case, they will be willing to reduce their margin to a loyal customer - but only because they know the market is low more often than not and that the customer pays above the baseline more often than not as well. It’s a quid pro quo.

What’s the best time to contract coffee this year?

Many people wonder whether they should contract coffee from Brazil now or wait for prices to drop. For a trader, this is the million-dollar question. Right now no one can tell - that is why people who specialize in this are called speculators. It’s not unreasonable to think, though, that the price of commodity coffee could go up again if it turns out that the frost damage is larger than expected. We’ll find out in September. The reverse is also a reasonable scenario. We don’t envy traders... It’s a gamble.

Our advice is to act now. If you need coffee from Brazil (or Peru, Colombia & Rwanda for that matter) to arrive before February you need to contract it fairly soon. If you are looking for something specific or exotic, get it booked before the end of September. These coffees are snapped fast. In 2019, we saw many roasters looking for Brazil Pulped Naturals in October. By then there were only naturals left as it was a smaller harvest. If you want the pick of the crop you have to be first to the stall.

How can I navigate this as a roaster?

Coffee producers are looking for direct relationships. They want to work with you. If you can offer the intention of continuing to work with them for several years they will work with you on the price and find a middle ground. Some might not, but we guarantee most will. You know that the extra money you are paying this year will go back to the farmers who will be producing coffee in years to come. If you think of how low prices have been in the recent past, this money is not going to be opportunistic profit. It will help farmers pay their debts, invest in their farms and produce better coffee as they should be able to do every year. You also win.

We would encourage roasters to talk to as many producers as they can. Even if you’re not buying coffee from them this year, talking to people from different areas of the coffee industry can really help widen your understanding of the full story. When you find a producer that shares your values and that you get on with, it’s magic and goes way beyond a price conversation.

In a general way, when you think about coffee prices you should think long term. The mindset of trying to get the best price now and just thinking about the current rates is a rather opportunistic one. It tries to maximise opportunity in the short term. The other possible mindset is to grow through relationships in which both parties look after each other regardless of what the market is doing. In this sense, what separates specialty from the C-market is not the coffee. It’s the nature of the relationship.

Stay awesome and keep sourcing great coffee!

Let Us Know What You Thought about this Post.

Put your Comment Below.